.png)

This article explains what the UK SRS requires, who it applies to, what it means specifically for food companies and their Scope 3 obligations, how it compares to the EU's Corporate Sustainability Reporting Directive (CSRD) for businesses operating across both jurisdictions, and what food businesses need to do now to be ready before the 2027 deadline.

The UK Sustainability Reporting Standards (UK SRS) are the UK's official framework for sustainability and climate-related financial disclosure. Published on 25 February 2026 by the Department for Business and Trade, they set out what companies must report about the sustainability risks and opportunities that could affect their financial performance. The standards are built on the global baseline developed by the International Sustainability Standards Board (ISSB), aligning the UK with over 30 other jurisdictions including Australia, Canada, and Japan that are adopting the same foundations for sustainability reporting.

The UK SRS replaces the TCFD-aligned disclosure rules that listed companies had been reporting under voluntarily since 2021. The TCFD (Task Force on Climate-related Financial Disclosures) was disbanded in 2023 after its recommendations were absorbed into the ISSB's global standards, the same standards the UK SRS is built on. Rather than creating something entirely new, the UK SRS builds on and expands those ISSB standards, requiring more granular climate-related financial disclosures, stronger connections to financial statements, and a clearer audit trail.

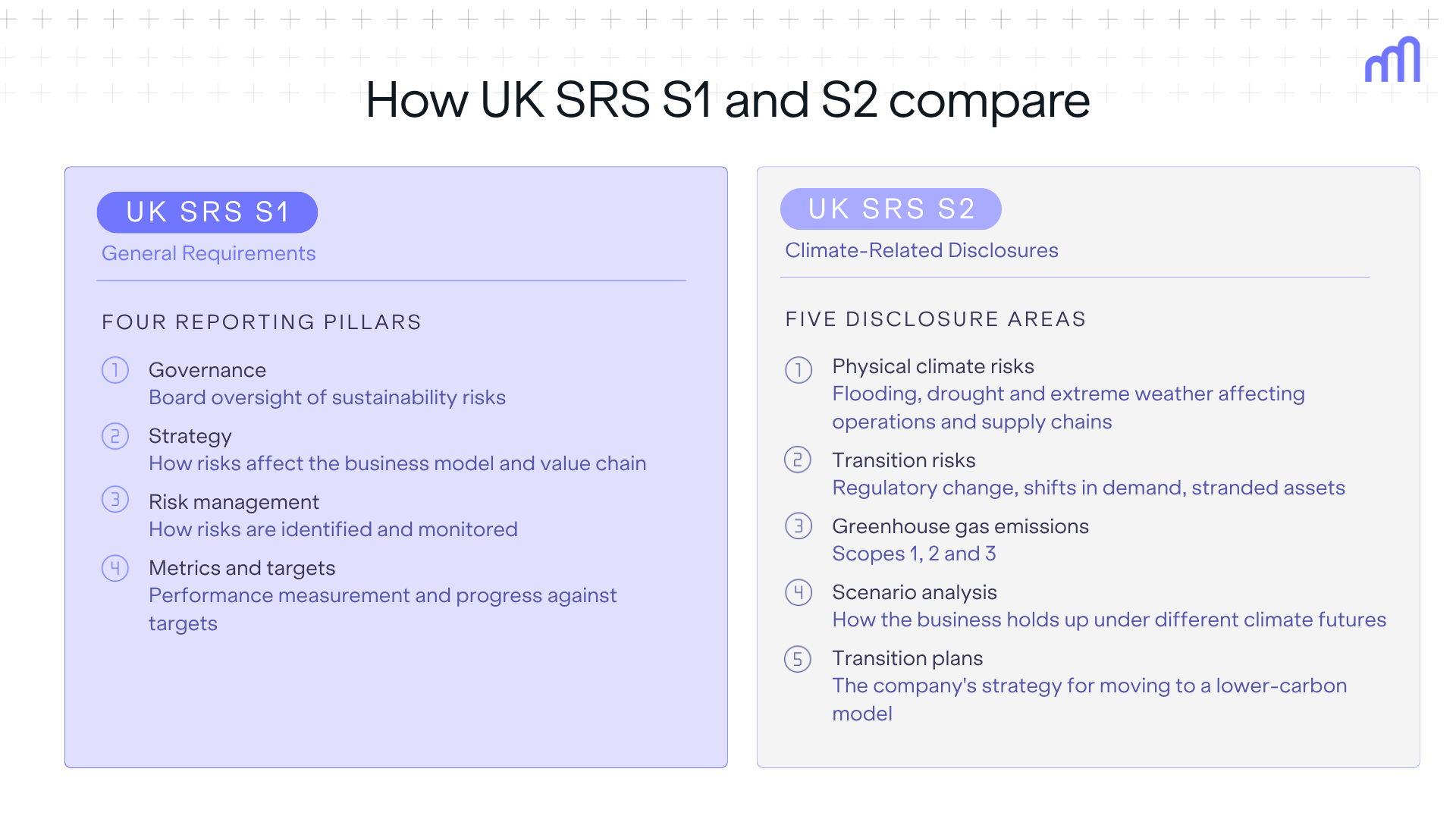

The framework has two components:

S1 is the overarching standard that applies to all sustainability-related risks and opportunities, not just climate. It requires companies to disclose anything that could reasonably be expected to affect their cash flows, access to finance, or cost of capital. Reporting is structured across four pillars:

One important requirement runs across all four pillars: S1 disclosures must be connected to financial statements. Sustainability reporting is no longer a standalone document. It needs to link directly to financial accounts and be supported by audit-ready data.

S2 deals specifically with climate. It requires companies to disclose:

S1 and S2 are designed to be applied together. A company reporting under S2 on climate must also apply the relevant parts of S1 to ensure those disclosures are properly structured, connected to financial data, and auditable.

For listed companies already reporting under TCFD-aligned rules, UK SRS is not a complete reset. The four-pillar structure (Governance, Strategy, Risk Management, Metrics and Targets) carries over directly from TCFD. What changes is the level of detail required. UK SRS S2 adds mandatory Scope 3 disclosure, quantitative scenario analysis, and explicit transition planning requirements that were recommended but not mandated under the previous TCFD framework. The bar for audit readiness is also significantly higher.

The Financial Conduct Authority (FCA), the UK's financial regulator, is responsible for translating the UK SRS into mandatory listing rules for companies on the London Stock Exchange. Its consultation paper CP26/5 proposes that mandatory reporting applies from 1 January 2027, covering five types of listed company:

For most food businesses reading this, UKLR 6 is the relevant category. If your company has shares listed on the London Stock Exchange Main Market, you are in scope.

Not everything comes into force at once. For UKLR 6 commercial companies, the obligations phase in as follows:

.png)

This phasing gives companies time to build up their reporting infrastructure, but the 2027 mandatory baseline is more demanding than it might appear. Full S2 climate disclosure requires scenario analysis, value chain mapping, and governance structures that many food companies do not yet have in place.

Private and unlisted companies are not directly required to comply under the current proposals. The government is consulting separately on whether to extend requirements to larger private companies, but nothing has been confirmed yet. That said, unlisted food businesses should not treat this as a reason to wait. Large listed customers and parent companies will need Scope 3 supply chain data to meet their own reporting obligations, meaning the data burden will cascade upstream through the value chain regardless of whether a supplier is listed or not.

For food businesses, the most significant part of UK SRS is what S2 requires on Scope 3 emissions. For most food and beverage companies, food supply chain emissions from agriculture, ingredients, and primary processing represent between 80 and 90 percent of their total carbon footprint. Under UK SRS S2, these emissions must be measured, disclosed, and supported by documentation that can withstand external scrutiny.

What makes this particularly demanding is how the standard expects Scope 3 to be measured. UK SRS S2 is explicit: companies should prioritise primary data, meaning supplier-specific emissions figures collected directly from the value chain, over secondary data like industry averages or spend-based estimates.

For a food brand with hundreds of ingredient suppliers across multiple geographies, that is a significant data collection challenge. Most food companies today rely heavily on secondary data for their Scope 3 calculations. UK SRS S2 sets a clear direction of travel away from that approach, toward verified, traceable, supplier-connected figures.

The data burden does not stop at the listed parent company. It cascades upstream through the supply chain across several tiers:

.png)

There is also the question of audit readiness. UK SRS S1 requires disclosures to connect directly to financial statements and be supported by verifiable, traceable data. For food companies that have built their carbon reporting on estimated figures and industry averages, closing that gap before the 2027 deadline requires meaningful investment in data infrastructure now.

For a practical guide to what audit-ready carbon data looks like in practice and how food companies can build a reporting infrastructure that holds up to regulatory scrutiny, read our article How to Build a Regulator-Proof Corporate Carbon Footprint.

The fundamental difference is how each framework defines what needs to be reported.

For food companies with operations, subsidiaries, or significant customer relationships across both the UK and EU, UK SRS is not the only framework to prepare for. The EU's Corporate Sustainability Reporting Directive (CSRD) applies to large companies operating in EU markets, and the two frameworks diverge in one important way.

UK SRS uses financial materiality: companies disclose sustainability risks that could affect their financial performance and investor decisions. The CSRD uses double materiality: companies must report not only on financial risks, but also on the impact of their operations on people, society, and the environment. In practice this means the EU requires a broader set of disclosures than the UK, covering social and environmental impacts that would fall outside the scope of UK SRS entirely.

For food companies caught by both frameworks, the challenge is not just reporting twice. It is building a data infrastructure that can serve two different standards simultaneously. The good news is that Scope 3 supply chain emissions sit at the centre of both. Getting your product-level emissions data right, with supplier-specific inputs and a clear audit trail, is the foundation that makes compliance with both frameworks possible. Companies that invest in that data infrastructure now will be far better placed to meet both sets of obligations as deadlines approach.

With mandatory UK SRS reporting proposed from January 2027, the window for preparation is shorter than it looks. The FCA's final rules are expected in autumn 2026, which means companies that wait for confirmed requirements before acting will have very little time to build the data infrastructure, governance processes, and supplier relationships that credible reporting requires.

For food companies inside or adjacent to the regulatory scope, five priorities stand out:

UK SRS S2 requires Scope 3 emissions to be disclosed across all 15 categories of the Greenhouse Gas Protocol (GHG) value chain standard, with a clear preference for primary, supplier-specific data over industry averages. If your current approach relies on spend-based estimates or sector-level emission factors, that is the first and most urgent gap to close. The question to ask is not just whether you have a Scope 3 number, but whether that number could survive external assurance.

UK SRS S1 requires companies to disclose where in their value chain sustainability risks are concentrated. For food businesses, that means mapping emissions and climate-related risks across ingredient sourcing, primary processing, packaging, logistics, and retail distribution. Companies that have never done this at a product level will find it takes longer than expected.

The primary data that UK SRS S2 prioritises largely comes from suppliers. Getting that data to a quality that supports auditable reporting requires time, trust, and often technical support for suppliers who have never been asked to report emissions data before. Starting those conversations now gives you the best chance of having usable data when reporting begins.

UK SRS S1 requires companies to disclose how their board oversees sustainability risks and opportunities, including whether sustainability performance is linked to executive remuneration. If climate risk is not yet on the board agenda in a structured way, that needs to change before 2027. This is not a reporting exercise. It is a governance one.

If your business is subject to both UK SRS and the EU's CSRD, a gap assessment against both frameworks now will surface where your data architecture needs to serve two different materiality standards. Building one system that satisfies UK SRS financial materiality and then retrofitting it for CSRD double materiality is significantly harder than designing for both from the outset.

For food companies working through what UK SRS means in practice, the data challenge is the hardest part. Carbon Maps is built exclusively for companies with complex agricultural supply chains, calculating product-level carbon footprints across entire portfolios using ingredient-specific emission factors. The kind of granular, supplier-connected data that UK SRS S2 prioritises over industry averages.

Every calculation produced by Carbon Maps is auditable and traceable back to its source, which matters when disclosures need to connect to financial statements and withstand external assurance. And because Carbon Maps works at product level rather than company level, food businesses can see exactly where in their value chain emissions are concentrated, across ingredients, processing, packaging, and logistics — which is precisely what UK SRS S1 requires companies to map and disclose.

Speak to our team to find out how Carbon Maps can help you build the emissions data infrastructure that UK SRS reporting demands.